UK central bank sees a gloomier winter than its earlier forecast | United Kingdom News

[ad_1]

The Bank of England slashed its economic forecasts for the United Kingdom on Thursday and boosted its already huge bond-buying stimulus programme.

The UK’s central bank increased the size of the stimulus by a bigger-than-expected 150 billion pounds ($195bn) as it prepared for economic damage from new coronavirus lockdowns and the looming risk of an exit from the European Union without a trade deal.

The move comes on the day that England entered a four-week lockdown to curb a second wave of COVID-19, which is now killing as many people in the country each day as it did in May.

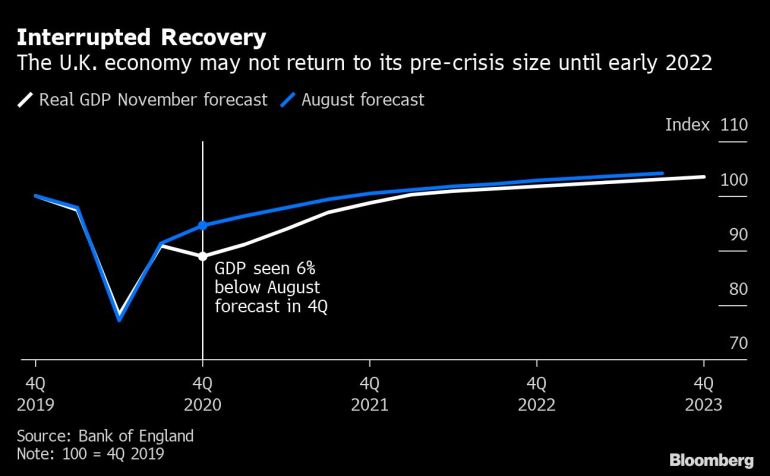

The BoE said the UK’s economy was set to shrink 2 percent during the fourth quarter as a result, and that the economy would shrink by a record 11 percent over the course of 2020 overall, more than the 9.5 percent it had forecast in March.

“The outlook for the economy remains unusually uncertain,” the BoE said.

“It depends on the evolution of the pandemic and measures taken to protect public health, as well as the nature of, and transition to, the new trading arrangements between the European Union and the United Kingdom.”

[Bloomberg]

[Bloomberg]

The BoE kept its benchmark Bank Rate at 0.1 percent, as expected in a Reuters poll of analysts, and made little mention of negative rates while a consultation with banks over the practicalities is under way.

The BoE raised the size of its asset-purchase programme to 895 billion pounds ($1.2 trillion), 50 billion pounds ($65bn) more than expected by most economists in a Reuters poll.

The central bank said that would give it enough firepower to stretch its buying of government bonds through to the end of 2021.

“An extraordinary economic shock warrants an extraordinary policy response,” said Ambrose Crofton, global market strategist at JP Morgan Asset Management.

“The resurgence of the virus in recent months will mean both the government and companies are once again turning to global capital markets to borrow large sums. The Bank’s purchases in these markets will help prevent borrowing costs rising,” he said.

Sterling rose against the dollar and the euro after the announcements. Bond yields fell.

Slower recovery, higher unemployment

The central bank now expects the UK’s economy to exceed its size before the COVID-19 pandemic struck only in the first quarter of 2022. Previously, the BoE had forecast the recovery would be complete by the end of next year.

Unemployment was set to peak 7.75 percent in the second quarter of next year, much higher than its most recent reading of 4.5 percent, the BoE said.

[Bloomberg]

[Bloomberg]

Gross domestic product was likely to grow by 7.25 percent in 2021, weaker than a previous forecast of 9 percent.

But its two-year inflation forecast remained unchanged at 2 percent, the central bank’s target.

“Our view is that inflation will be closer to 1.5 percent by the end of 2022. That’s why we believe the Bank will still have to increase its policy support,” Ruth Gregory, an economist at Capital Economics, said.

The British economy has been supported by a surge in debt-fuelled spending by the government. The BoE is buying up many of those bonds.

Finance Minister Rishi Sunak is due to speak in Parliament later on Thursday about his huge support for the economy.

Despite the spending, the UK faces the worst peak-to-trough contraction of any Group of 20 economy, Moody’s said on October 16 when it cut the country’s credit rating.

The UK also faces the risk of a trade shock when its post-Brexit transition with the European Union expires on December 31.

So far, London and Brussels have failed to strike a new agreement. The BoE’s Monetary Policy Committee (MPC) said trade would suffer even if there is a deal.

“There is uncertainty around the extent to which the initial adjustment to new trading arrangements with the EU will affect activity,” the BoE said.

“The MPC’s projections are also conditioned on the assumption that cross-border trade falls temporarily in the first half of 2021 as businesses adjust to the new trading arrangements with the EU.”

Firms switch to temporary staff

Meanwhile, a survey published on Thursday showed that British employers cut their hiring for permanent positions for the first time in three months in October and relied increasingly on temporary staff in the face of a second wave of coronavirus restrictions.

The growing number of people looking for work pushed down starting pay, and the number of vacancies posted by companies seeking to hire workers fell slightly, the Recruitment and Employment Confederation (REC) and accountants KPMG said.

Firms appeared better prepared to operate through the new restrictions than they were in March, but the outlook was concerning, REC Chief Executive Neil Carberry said.

“We face a challenging winter and temporary work will be a vital tool for keeping businesses going and people in work,” he said.

The REC/KPMG measure of temporary hiring hit its highest level since December 2018.

To slow a rise in unemployment, Britain’s government on Saturday extended for one month its broad job subsidy programme, which pays 80 percent of the wages of temporarily laid-off employees, after ordering a new four-week stay-at-home lockdown for England which begins on Thursday.

“While the furlough scheme extension may give a brief respite, it will fuel economic uncertainty and further dampen prospects for job-seekers, hitting hiring activity hard,” James Stewart, vice chair at KPMG, said.

[ad_2]

SOURCE NEWS